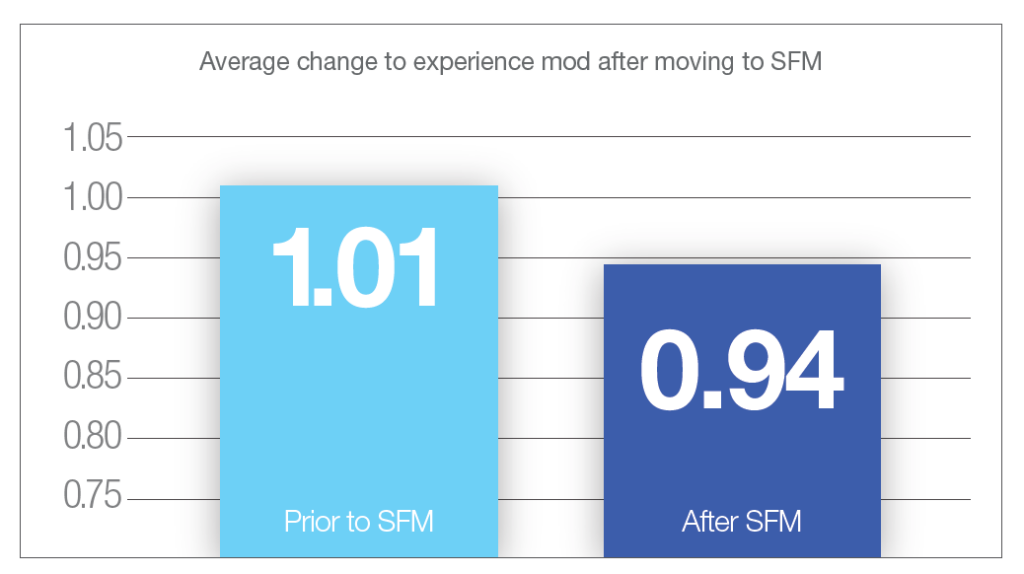

Did you know that large policyholders who switch to SFM see on average a 7-point reduction in their experience modification (e-mod)?

Check out this chart for the specifics:

This chart shows SFM policyholders with $50,000 or more in manual premium that qualified for an experience modification factor. Each of these policyholders had continuous workers’ compensation coverage with SFM through a minimum of five policy terms: 1.01 prior to SFM and 0.94 after SFM.

How does SFM achieve such success for its customers? There are several reasons, including our approach to loss prevention and claim management.

Claim management

- Low caseloads per adjuster

- 24/7 nurse triage for injury reporting

Loss prevention

- In-person services and training

- Online safety resources

Cost containment

- PPO networks

- In-house bill review

Workers’ compensation expertise

- Focused approach

- Leaders in the industry

Learn more about how we can help you get the most from your workers’ comp coverage.